Pinpointing the most reliable and most profitable short-term SPY trades since 2011

The following is a reprint of the market commentary from the July 2017 edition of The Option Advisor, published on June 22. For more information, or to subscribe to The Option Advisor -- featuring 10 new option trades each month -- visit our online store.

"...the SPDR S&P 500 ETF (SPY) has the most liquid options market of any ETF or even stock. The world's largest exchange-traded fund, with $237 billion in assets under management (AUM), currently has 17.8 million options contracts outstanding... Bid/ask spreads on SPY options are often no more than a penny wide, minimizing transaction costs for those who want to hedge or speculate on the S&P 500."

-- ETF.com, "15 ETFs With The Most Liquid Options," June 21, 2017

Even prior to reading the excerpt above, it's quite likely you were aware of the dominance of SPDR S&P 500 ETF (NYSEARCA:SPY) calls and puts. The fund, which tracks the benchmark S&P 500 Index (SPX), regularly appears at the top of daily "most active options" lists, and SPY puts are frequently recommended to those looking to hedge long equity exposure in one fell swoop.

But how do SPY options really perform for investors? For those using SPY purely for hedging purposes, the answer to this question might seem irrelevant; after all, the best-case scenario for any insurance policy is that you never need to use it. But for those interested in speculating on short-term SPY moves via calls and puts, we'll attempt here to determine -- through some significant number-crunching by our Senior Quantitative Analyst Rocky White -- what kind of results traders can expect from different SPY option strategies.

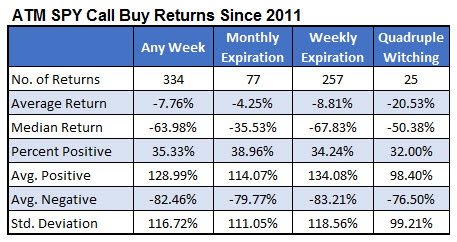

When trading an asset with such a wide variety of available strikes and expiration dates as SPY, the number of variables in constructing an options trade can be dizzying. For the purposes of this study, we narrowed our focus to one-week returns on at-the-money SPY calls and puts, with the hypothetical trades initiated at the close of trading on Friday and exited the following Friday (or the last day of the trading week, in the event of a holiday). We then broke down the results to compare "traditional" monthly options returns against their weekly counterparts, to gauge whether one class outperformed the other -- and as such, we ran data back to 2011, which is the first full year of SPY weekly options data.

We further segregated "quadruple witching" expiration weeks -- like the one we just concluded in June -- into a class of their own. It's worth stipulating here that SPY returns during quadruple witching weeks average just 0.24% and 60% positive, versus the SPX's more robust 0.74% average return and 68% positive, due to SPY's quarterly dividend payout -- an extenuating circumstance accounted for by the corresponding SPY option premiums, as is to be expected. Also worth noting are the lagging SPY returns during monthly expiration weeks (0.16% on average, versus 0.30% for the SPX).

Diving into the options data itself, SPY call buying is a fairly dismal approach during quadruple witching week. The average at-the-money SPY call option return of a 20.53% loss is far worse than the average "any week" return of -7.76% -- despite the average SPY return of 0.24% for quadruple witching arriving right in line with the "anytime" weekly return of 0.22%.

And this divergence doesn't appear to be a function of pumped-up implied volatility (IV) heading into quad witching, either. The average IV since 2011 for SPY ATM calls was 16.9%; looking exclusively at quadruple witching weeks, it's only slightly higher at 17.1%.

Given this notable call option underperformance, can we conclude that selling SPY calls every quadruple witching expiration week is a "no brainer"? Per the table below, it does seem that the quarter-end expiration week is the best time to implement a one-week SPY call selling strategy. While the "wins" on sold calls are modest across the board, the quad-witching call sells are the most likely to yield a positive return (68% of the time). The average positive return is the lowest during quad witching week by a very slim margin, but the average negative return is also the smallest -- yielding a net average return of 0.99% for these weeks, which comfortably outpaces the other weeks of the trading year.

As for SPY put buying, it's a similar scenario to the call buying outcomes detailed above. The percentage of positive returns is uniformly slim -- ranging from a low of 16% during quad witching to a high of 23.35% in weeks outside of standard monthly options expiration -- which indicates a high probability of a losing trade.

That said, when SPY puts pay off, they pay off big. The average positive return for a profitable SPY put exceeds that of purchased calls during every week, ranging from an average positive gain of 116% during quad witching to nearly 182% (close to a triple) during monthly expiration weeks. For traders with high conviction that SPY will sell off during the course of any given week, a short-term options trade can be quite profitable.

Finally, in terms of both win rate and average return, SPY put sells offer the best odds for short-term options traders. The percentage of positive returns tops out at 84% during quadruple witching week, but falls no lower than 76.65% in non-monthly expiration weeks. What's more, the average returns on at-the-money SPY put sells consistently outpace comparable returns on SPY call sells. For those traders who prefer a high win rate in exchange for modest overall returns, a SPY put selling strategy typically fits the bill.

Of course, the appropriate SPY options strategy will primarily depend upon the technical outlook for the ETF over the time frame of the trade. And that's where it's important to remember that, due to its outsized popularity among options traders, SPY is highly susceptible to the influence of heavy call and put open interest strikes -- particularly during monthly expiration, when open interest accumulations are often at their largest. Accordingly, any trader considering a short-term SPY trade would do well to include a careful analysis of the fund's relevant open interest configuration before opening a short-term options trade -- whether it's a purchased put, a sold call, or any alternative in between.