The inverse volatility ETN could be signaling an imminent pop in the VIX

We've previously discussed the usefulness of the VelocityShares Daily Inverse VIX Short-Term ETN (XIV) -- which is designed to move in diametric opposition to the CBOE Volatility Index (VIX) on a daily basis -- for purposes of analyzing stock market volatility from a more technical, pattern-driven perspective. And when XIV shows signs of being overextended, it's reasonable to consider the notion that XIV (and, potentially, the stock market) is due for a pullback -- which would naturally coincide with a VIX spike.

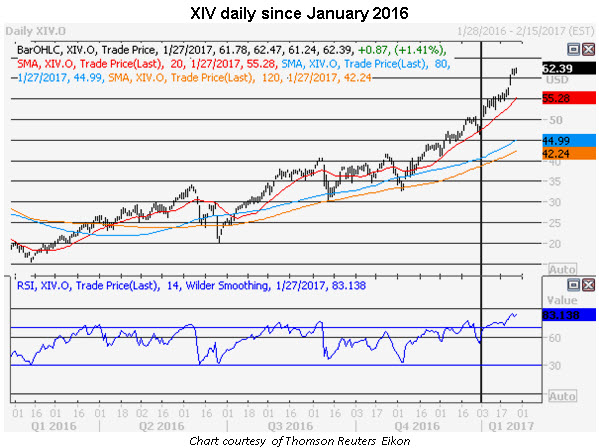

As it happens, "overextended" would be a fair way of describing XIV's current state. There have been nearly $77 million in XIV outflows year-to-date, per etf.com, as the exchange-traded note has broken out to record highs alongside stocks against the backdrop of a remarkably tame VIX. XIV is now docked well above its 2015-2016 highs around the $50 level, and -- as of Friday's close -- was perched at a lofty $62.33. In fact, XIV peaked north of $62 in each of the last three trading days, a level at which the shares have more than quadrupled their February lows, and more than tripled their post-Brexit June lows.

To put it in more concrete terms, we'll define "overextended" as occasions where XIV (a) closes 10% or more above its 20-day simple moving average; and (b) has a 14-day Relative Strength Index (RSI) of 70 or greater. There have been 13 such signals since XIV started trading, with the first recorded in 2011. Per the tables below (click to enlarge), courtesy of Schaeffer's Senior Quantitative Analyst Rocky White, an overextended XIV doesn't necessarily signal an imminent plunge for XIV or equities.

In fact, the average S&P 500 Index (SPX) returns after an "overextended XIV" signal outperform the index's "anytime" returns over one-week, two-week, and one-month time frames. Meanwhile, XIV's post-signal average returns outperform the comparable anytime figures across every time frame we studied. And for both S&P and XIV, the volatility of returns (as reflected by standard deviation) is considerably lower than usual after one of these signals.

While the post-signal results above should be reassuring for bulls, we must also consider the average VIX returns after one of these "overextended XIV" occurrences. After one of these signals, the VIX displays higher-than-usual average returns across each of these short-term time frames, relative to its at-any-time performance. VIX's median returns are positive over three of the four time frames after a signal, compared to consistent declines over comparable anytime periods. Likewise, the "percent positive" is higher over every period. The disparity is particularly noticeable in the three-month column; note that VIX's average return post-signal is 14.52%, and is positive 83.3% of the time. By contrast, over a typical three-month time frame, VIX is higher only 45.2% of the time, with an average return of only 3.37%.

Based on this analysis, investors may not need to prepare for a brutal sell-off in stocks -- but they may be well-served by preparing for a volatility pop in the coming weeks and months. Or, as Senior V.P. of Research Todd Salamone recently observed about an entirely different set of data points, "... the best conclusion is that stocks do not have the same magnitude of downside risk at the moment relative to the upside volatility risk."

Subscribers to Bernie Schaeffer's Chart of the Week received this commentary on Sunday morning. Sign up for this free weekly newsletter to get exclusive early access to Bernie's latest research.